Give to Get Data Businesses

Burgiss, Preqin, STR, Tegus, eVestment, Pave: what these data businesses have in common

What makes a data business valuable? Durable? A multi-decade enterprise? In this piece I’ll highlight a handful of give-to-get (“GTG”) data businesses, and what led to their rise. We’ll look at Burgiss (sold to MSCI for $913m), Preqin (sold to BlackRock for $3.2b), STR (sold to CoStar for $450m), Tegus (sold to AlphaSense for $930m), eVestment (sold to Nasdaq for $705m), and Pave (raised at a $1.6b valuation). These businesses are extremely difficult to disrupt. They take decades to build, and once in place, typically win their entire market.

Put simply, a GTG data business is one that aggregates inputs from a fragmented market, and sells the resulting data back to that same market. Often these GTG businesses require data contribution in order to receive the aggregated information. A strong GTG business acts as a central hub for a particular industry, interacting with hundreds, or thousands, of market participants:

The most valuable GTG businesses operate in fragmented industries (thousands of players), where participants have temporal, mission critical data that they use to make key business decisions. For example, the private asset management market (LPs, asset managers) have strong fundamentals for a GTG business. On one side sit the funds: more than 18,000 private equity funds and 1,700 venture capital funds in the US alone.1 On the other side sit thousands of institutional LPs (public pensions, endowments, sovereigns, insurers). Both sides need data: GPs to benchmark themselves, LPs to evaluate the GPs.

A key aspect of the GTG loop is that the value of the GTG data asset increases over time as more participants contribute to it. This increases the customers’ reliance on the aggregated data, and the actionability of the data. For example, hotels price rooms and measure manager performance based on weekly STAR Reports, pension funds invest billions of dollars based on manager performance on eVestment2, and tech companies base comp decisions on Pave benchmarking reports.

Neutrality

There’s one aspect that makes or breaks the loop: the GTG entity has to be trusted by the market participants it reports on. A GTG business asks competitors to hand over their most sensitive numbers (room rates, fund returns, salary bands) then sells a version of that data back to them. The loop only works if contributors believe the aggregator is neutral and won’t favor certain participants. Burgiss built its universe from LP-reported figures precisely because GP self-reporting was biased (GPs stop reporting their poor returns), which let it publish honest numbers without fear of offending the funds it covered. STR anonymizes every hotel into a competitive set and leaned on industry endorsements to build its authority. eVestment vetted the returns managers submitted, which is what made consultants trust it.

Stripped down, the businesses that compound share five traits:

A fragmented market: thousands of participants, none of whom own the majority of the data.

Mission-critical, temporal data: the data is time sensitive, and real decisions rely on the latest information.

A trusted, neutral hub: data contributors believe the aggregator won’t compete against them.

A growing market: the data will become more valuable as the underlying market expands.

A path to becoming a data currency: the data ends up written into the contracts and transactions of the industry.

The six businesses

Burgiss

Preqin

Smith Travel Research (STR)

Tegus

eVestment

Pave

Burgiss

History

Burgiss was founded by James Kocis in 1987. Kocis had just wrapped up four years as a Project Manager for the New Jersey Meadowlands Commission when he bought his first computer:

In 1983, bought an IBM PC from Computerland on Route 22 with my dad. Father and son became partners. Helped lead several computer user groups in NJ and NYC. Taught computers to adults and wrote and published training guides. Formed a company, the Burgiss Group.3

Kocis started to create private equity databases during a consulting project:

In 1993 I was at my wits’ end trying to keep track of well over a hundred partnerships. Then I met Jim Kocis. He had approached Mitchell Hutchins about developing a Windows version of a private equity system to little avail. Then Jim came to see me and I said that AT&T would put up $25,000 a year for a few years to develop such a system. The rest is history. Today the Burgiss Group helps over 200 clients monitor and manage billions of dollars of private equity assets.

— Tom Judge (p. xv)4

Kocis created the Burgiss Group, which became the ultimate system of record for private equity LP’s. Users could track their investments, analyze fund returns, benchmark asset managers, and generate various reports.

A snapshot of Burgiss Private i from 19985:

Timeline

1987: The Burgiss Group was founded

1993: Developed Private i (record-keeping software)

1999: Added data operations

2006: 185 customers6

2009: Private i customers were using the software to manage over $1 trillion of investments (p. xxv)4

April 2011: Launch of Private iQ (co-op/benchmarking layer built on top of Private i data)

2016: Over 1,000 clients, over $2 trillion in investments monitored7

2018: Burgiss tracked “more than $5 trillion in private capital.”8

Jan. 2020: MSCI minority investment of $190M for 34% stake9

2021: Burgiss acquired Caissa (portfolio analytics company) for $26m10, hit 450 employees combined11

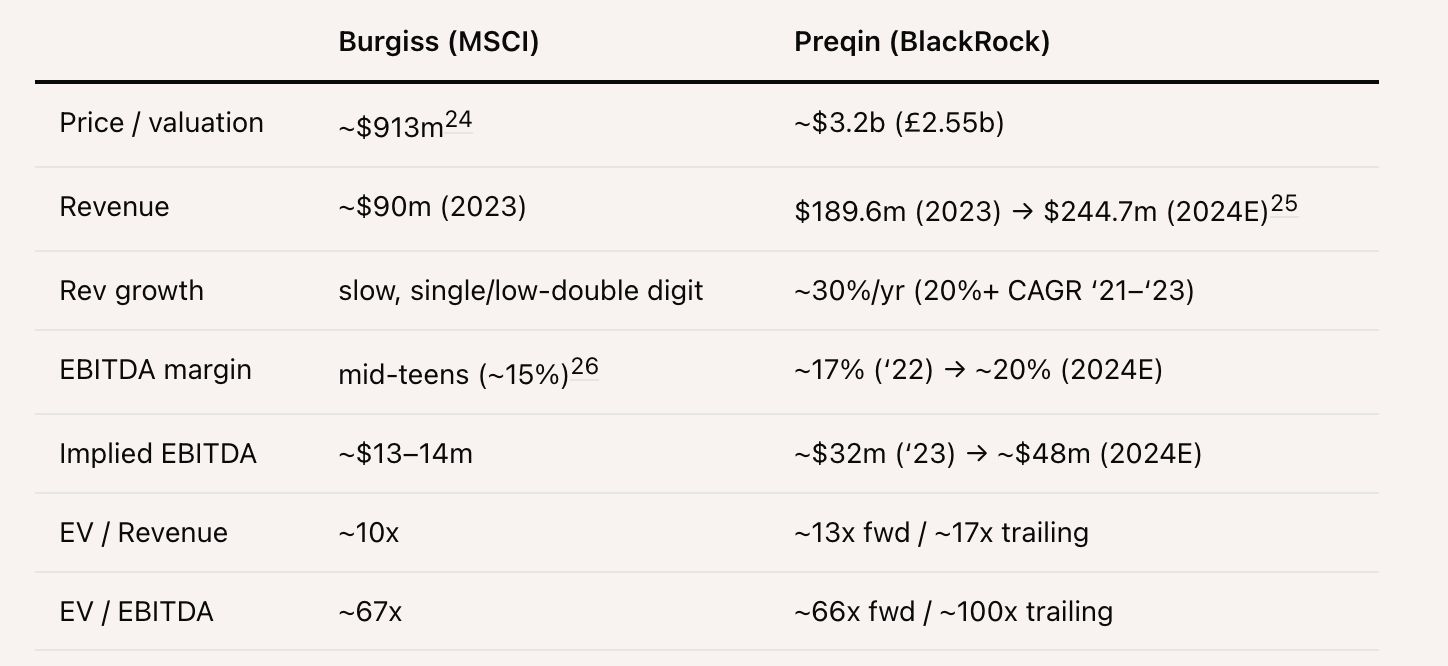

Oct. 2023: MSCI completes purchase of Burgiss, total consideration of $913m to complete deal12

“Burgiss is expected to generate over $90 million of revenue in 2023 with an EBITDA margin and operating income margin in the mid-teens.”13

The Burgiss Universe

Burgiss had a structural advantage: its data was sourced primarily from LPs, not GPs, and LP data is the most accurate record of private fund performance. GP-reported data skewed upward: GP’s stopped reporting once they had poor returns, so any benchmark built on GP self-reporting was biased. Unlike the consulting firms it competed with, Burgiss was a neutral ground for accurate information. They could report the honest numbers on GP performance (sourced from LPs) without fear of offending a GP, since their clients were mainly LPs.

A typical Burgiss customer not only bought their investment management software from Burgiss (Private i), but they also supplied the data that contributed to Burgiss’ corpus (Private iQ). In return, they got peer group benchmarking. This is a classic GTG loop: the benchmarking is only useful if the “data universe” is complete, the universe is only complete if LPs contribute lots of data, LPs only contribute because the benchmarking is useful. Each new LP made the dataset more complete, which made the benchmarking more useful, which incentivized the next LP to want access and contribute its data. Burgiss charged tiered annual subscription fees based on AUM and/or number of investments.

Burgiss’ competitors “sub-universes”

Kocis, the founder of Burgiss, co-authored a textbook “Inside Private Equity: The Professional Investor’s Handbook” in 2009. Interestingly, he laid out the flaws in many of Burgiss’ competitors (Sand Hill Econometrics, Thomson Reuters TVE, Cambridge Associates, and Preqin), two years before the release of Private iQ:

From our vantage, the current state of commercially available information about private equity is a mess. We are acutely aware that universe data about private equity is rightly hard to get, assemble, maintain, and audit. We believe that the industry is currently poorly served, and we are not alone in our criticism.(p. 126)4

What MSCI saw in Burgiss

MSCI’s core business is selling benchmarks/indexes for public markets. MSCI has an incredible data-currency moat: trillions are benchmarked to their indexes, asset managers are measured against them, products track them, and MSCI collects a tax on their use. Two or more parties rely on an MSCI index to transact, and MSCI collects a toll along the way.

What MSCI never had was a private-markets equivalent. Post-acquisition, MSCI quickly used its newfound data from Burgiss Private iQ to create hundreds of new benchmarks and indexes.14 Burgiss had the most complete + accurate database for this type of product.

It looks like MSCI is trying to strengthen Burgiss’ GTG moat by layering a data-currency on top, with all of its new private markets indexes.

Preqin

“Preqin’s performance data are sourced primarily from public filings by pension funds, from FOIA requests to public pension funds, and voluntarily from GPs (about 60% of performance data) and LPs.”15

History

Preqin was founded in London in 2003 by Mark O’Hare and Nick Arnott as “Private Equity Intelligence.” Prior to Preqin, the two had co-founded CityWatch, a data business that provided share ownership information on UK businesses (acq. by Reuters for £2.5m in 1998).16

Timeline

2003: Founded in London as Private Equity Intelligence; begins collecting fund performance via FOIA17

2009: Rebrands to “Preqin” as it expanded across alternative asset classes

June 30, 2024: BlackRock agrees to acquire Preqin for £2.55b (~$3.2b) in cash18

At the time of the BlackRock deal, Preqin had 4,000+ clients and ~$240m of recurring revenue (it sold for ~13x revenue).19 Notably, Preqin compounded for two decades without raising outside equity capital.

The Wedge

While Burgiss used software as its wedge to acquire the data (selling LPs a system or record and accessing the data that flowed through it), Preqin brute forced most of its data:

[Preqin] obtains much of its information from sources that are under forced dis-closure, such as Freedom of Information Act (FOIA) requests.(p.117)4

Since 2002 Preqin has pulled performance figures from public pension funds (CalPERS, Washington State Investment Board, Florida State Board of Administration, and many others) that are legally obligated to disclose them.20 Preqin was able to use FOIA to solve its cold-start problem.

Preqin is more aggregator than give-to-get

Preqin is best understood as a brute-force aggregator with a thin GTG layer on top. Its base is FOIA filings and public records, but on top of that base it added a voluntary contribution loop. Today Preqin draws performance from four channels: GP quarterly reports to LPs, FOIA, voluntary submissions, and public data, with 2,200+ fund managers now contributing.21

If you’re a GP and Preqin only has your FOIA’d figures, allocators see a partial, possibly stale picture. GPs are therefore incentivized to submit to Preqin, and they get to control the narrative and stay discoverable (not as tight of a loop as Burgiss’s).

Mission critical, temporal

Private fund performance is less temporal than hotel rates, or salaries (fund performance is often quarterly and lagged), but it’s mission-critical. LPs invest billions and benchmark a fund’s IRR/TVPI against Preqin (or Burgiss) data.

What BlackRock saw in Preqin

BlackRock framed Preqin as the data complement to its Aladdin/eFront products, and estimated private-markets data as an ~$8bn TAM growing 12% a year to $18bn by 2030.22 BlackRock/Preqin are in direct competition with MSCI/Burgiss in their desire to bring indexing to the private markets:23

“We believe we could index the private markets,” Fink said on a call with investors and analysts on Monday after the New York-based money manager announced the £2.55 billion ($3.2 billion) deal. “Just as index has become the language of public markets, we envision we could bring the principles of indexing even iShares to the private markets.”

Smith Travel Research (STR)

Smith Travel Research (“STR”) was founded in 1985 by husband and wife Randy and Carolyn Smith. The business started out by building a directory of thousands of hotels in the U.S., but quickly transformed into the hospitality industry’s largest data co-op:

So, we bought two PCs and a printer and for the next year, we put in 14-hour days seven days a week developing our Census Database. Soon after, I met with executives at Holiday Inn who were interested in the market share program I had talked about at L&H. Long story short, I spent a week in Memphis with Holiday Inn, and by the time I left we had outlined what would become the STAR report. Within a few months, I signed Hilton and Sheraton and got the endorsement of the American Hotel Association. With that, we were off and running, surveying 5,000 to 6,000 hotels across the country.27

Timeline

1985: Smith Travel Research founded, Census Database launched 28

1988: Launched the Smith Travel Accommodations Report (STAR)

March 2008: STR Global formed in London via merger with Deloitte’s HotelBenchmark and The Bench

2008: Launched HotelNewsNow.com

2008: 100 employees in Nashville, 30 in London 29

2013–2014: Acquired RRC Associates (research/consulting firm)

2019: Launched dSTAR dashboard (interactive benchmark product, later renamed STR Benchmarking in 2023)

October 2019: Acquired by CoStar Group for $450M cash. At close: $64M revenue, $16M EBITDA (7x revenue, 28x EBITDA), 370 employees, 66,000 hotels / 8.9M rooms / 180 countries30

2023: 78,000 hotels / 10.3M rooms / 2,595 submarkets tracked; >16,000 hotels actively contributing data, 1.2M STAR reports distributed monthly, renewals “in the high 90 digits”31

The Wedge

Randy Smith had to solve the difficult cold start problem that all data co-ops face. He solved this by using his credibility from the industry, and signing large franchise clients to get a lot of inventory onto the platform as soon as possible. Randy came from the hotel industry: prior to starting STR, he worked at a large franchisee of Holiday Inns (United Inns), and at Laventhol & Horwath (L&H) (an accounting/consulting firm) for a decade, building out various internal surveys. He eventually became director of research at L&H, tracking the performance of hotels around the country. 32

Randy and Carolyn signed Holiday Inns, and their franchisees, very early on. This was huge in solving the cold start problem. They also secured an American Hotel and Lodging Association (AH&LA) endorsement 33, had credibility from Randy’s decade+ in the hotel industry, and implemented strict anonymization when republishing their data.

The Product

The STAR Reports’ key features are:

Compset (competitive set: anonymized set of hotels that compete with the STAR recipient’s hotel) 34

ADR (average daily rate: calculated by dividing room revenue by rooms sold)35

RevPAR (revenue per available room: calculated by dividing room revenue by rooms available - occupied and unoccupied)36

STR’s value prop is its ability to aggregate and anonymize these metrics (+ more) across the entire hotel industry. STR helps hotels benchmark their locations, and understand room pricing (which, in the hotel industry, is volatile):

Another aspect of STR’s dominance is the fact that its data is written into hotel contracts. For example, some hotel management agreements give owners the right to terminate operators if the hotel’s RevPAR falls below a set percentage of its STR competitive set. Franchise documents and loan covenants are built on top of STR data. STR not only has a strong GTG moat, it also functions as a data-currency layer (transactions occur based on its published benchmarks and data).

2024 Class Action Complaint

We can find strong evidence of the strength of STR’s business in the lawsuit Portillo v. CoStar (W.D. Wash., 2024) . A class of hotel guests argued that STR was a hub-and-spoke price-fixing scheme: hotels feed their sensitive pricing data to STR, STR hands back the comp-set data, and that shared data allegedly let rival hotels push room rates higher than they otherwise could have. The complaint37 and case documents provide some great insight into how STR operated. For example:

By October 2023, Costar reported that more than 16,000 hotels were providing STR with forward-looking data, with Florance stating that “the more hotels we have contributing, the better data we are able to provide to the industry.” (compl. ¶ 15)

Every major hotel chain and many independent owners and operators around the globe—approximately 78,000 hotels in total-receive STR’s benchmarking reports. (compl. ¶ 65)

For the purpose of reporting, STR collects three types of confidential data from hotel competitors: rooms available, rooms sold and room revenue. Each participating hotel submits granular data broken down by type of travelers (transient, group and contract) and source of revenue (room, food and beverage revenue and other). STR refers to such data as “segmentation revenue.” (compl. ¶ 69)

In August 2025 the court dismissed the complaint (with leave to amend).

Acquisition:

STR was acquired in 2019 by CoStar for $450 million, in an all cash deal. Revenue was $64 million, EBITDA was $16 million. 28x EBITDA, 7x revenue, 370 employees.38 Prior to the STR acquisition, hospitality was a gap in CoStar’s CRE data platform. Similar to MSCI w/ Burgiss, CoStar was able to plug its asset-class hole with an acquisition.

Tegus

History

Tegus was founded in 2016 by twin brothers Thomas (Tom) Elnick and Michael (Mike) Elnick. Mike was an early employee at AlphaSights, a London-based expert network, so he had seen the incumbent’s business model from the inside. They spent 18 months pre-product before they settled on the business idea for Tegus.39

After 18 months of struggling to get traction, Tom and Mike flipped the script. They decided to start selling before they built anything. They’d ask funds to sign purchase orders and commit real money as part of their discovery conversations. That’s how they could discern “nice to have” from “need to have.” This approach scaled to every new offering. When Tegus started covering private companies, they followed the money and only built where clients were willing to pay.

— Bob Casey40

Initial competitors

The incumbent expert networks were GLG (Gerson Lehrman Group), AlphaSights, Guidepoint, Third Bridge, and Coleman Research. All ran the same model: source an expert, charge the client $1,000+ for a private call, take a fee, and let the client keep the transcript to themselves.

The wedge

Traditional expert networks sold alpha. Customers paid high prices (per call) hoping for a private, proprietary insight. The transcript was exclusive to the payer. Tegus fundamentally changed the pricing model. They came to market with a subscription pricing model. They realized that they could lower expert call prices, and sell a premium membership to the data corpus that resulted (squeezing their competitors’ margins in the process).

Tegus then followed the standard arc of a scaled data business: a small pool of buyers pays for data as a source of advantage. As the provider scales, data pricing drops and volume grows. Buyers largely stop paying for advantage (alpha), and start paying just to keep up with their competitors (beta). A great data business eventually becomes a tax on the market that it serves.

Pricing

Subscription: priced on fund AUM, roughly $20–25k per user/year, with contracts ranging from ~$25k to $150k+ depending on seats and modules.41

Timeline

July 2017: Raised Series A from IGSB ($1.5m at $4.5m post)

Jan. 2019: $1m ARR

Jan. 2020: $5m ARR

Jan. 2021: $13m ARR

Oct. 2021: Acquired BamSEC (an SEC filing data provider)42

Jan. 2022: $45m ARR

Aug. 2022: Acquired Canalyst (a pre-built financial model provider)43

Jan. 2023: $100m ARR

June 2024: Acquired by AlphaSense for $930m44

The thinnest moat?

One could argue that Tegus’ moat is the thinnest of the six businesses outlined here. The half life of its data (expert transcripts), is quite short. Tegus must constantly refresh its library to stay relevant to its customers. There isn’t much of a temporal compounding effect present in the transcript library itself. On the positive side, the dataset may become more useful due to advances in LLM’s.

What AlphaSense saw

AlphaSense is a market-intelligence firm. Its product is only as good as the proprietary content it can search. Buying Tegus took the best independent transcript library (100k+ calls), 4,000+ company models, and deep private-company (35k+ companies) coverage off the board and fed them into AlphaSense’s engine.45 The acquisition was a content-and-consolidation play to power AI search.

eVestment

History

eVestment was founded in 2000 in Atlanta by four ex–Watson Wyatt (an institutional investment consulting firm) employees: Jim Minnick (CEO), his wife Karen Minnick, Matt Crisp, and Heath Wilson.

eVestment was founded in 2000 because my co-founders and I, working with institutional investment consulting firm Watson Wyatt (now Willis Towers Watson), realized there was a better and more efficient way to collect, disseminate, analyze and create value from all the institutional investment data that investors, consultants and managers used every day in their work.46

Timeline

2000: Founded in Atlanta as eVestment Alliance

2007: Released Omni, a way for managers to populate 60+ databases at once47

2008: Insight Venture Partners makes an equity investment

2010: SVB extends a $19M credit facility

Sept. 5, 2017: Nasdaq announces $705M all-cash acquisition48

Oct. 23, 2017: Deal closes at ~8.7x revenue, ~16.5x 2018 “adjusted cash” EBITDA. At acquisition, eVestment had 2,000+ clients - including 92% of the top asset managers, 76% of the top consulting firms, and 70% of the top-20 pension funds. The disclosed numbers imply “adjusted cash” EBITDA in the 40-50% range.49

The wedge

Asset managers paid nothing to submit their performance data. Their incentive for submitting was because that’s how they were seen by consultants (who would then drive $ to them). eVestment then charged managers for visibility and analytics, including who viewed their profile, so they could market to interested consultants, and consultants paid for access to the full dataset.50

The reason this loop worked is because it all centered around the asset allocation decision. Consultants advise pension funds on which managers to hire, the consultants screen managers in eVestment, so managers must be in eVestment, with accurate data, to be considered at all. eVestment vetted the managers’ submitted returns, which is what made the consultants trust the platform.

A requirement

Public pension funds and their consultants eventually required managers to maintain their returns in eVestment as a precondition to being evaluated51:

Pricing

Asset managers paid to be listed.

Consultants paid for access to data.

Who buys the data

Asset managers (visibility + analytics + Omni), investment consultants (access for manager due diligence and selection), and asset owners (pensions, sovereigns, endowments) (monitoring and search).

Mission critical, temporal

Data is updated quarterly for traditional managers (monthly for hedge funds/alternatives). This is less temporal than hotel room rates or salaries, and most similar to Burgiss/Preqin’s private-fund data. It’s absolutely mission-critical: managers are selected based on their performance in the eVestment peer universe.52

Pave

Pave’s GTG loop

To use Pave’s benchmarking, a company integrates its HR systems (HRIS, applicant tracking, cap table tools), and lets Pave pull its compensation data directly. Pave then aggregates and anonymizes the data into its shared corpus. You give your comp data to get everyone else’s. Each new customer makes the benchmarks more complete, which increases the value of the data for everyone else.53

The wedge

Matt Schulman (ex-Microsoft/Google SWE) founded the company as “Trove” in October 2019.54 The first product features were a virtual offer letter and a total compensation portal that showed each candidate the full value of their comp package/offer.55 Tech and VC backed employers were the ideal wedge because they had high comp, and highly variable comp (heavy equity), so the benchmarking problem was most valuable.

History

Founded in October 2019 by Matt Schulman. Prior to founding Pave, Schulman was a SWE at Microsoft and later Google.56

October 2019: Company founded as “Trove”

March 2020: Raised $890K pre-seed

December 2020: Rebrands to Pave. $16M Series A led by A16z57

March 2021: Launches real-time compensation benchmarking via direct integrations with HRIS, ATS platforms58

August 2021: $46M Series B at $400m valuation59

June 2022: $100M Series C at $1.6b valuation, acquired Option Impact60

September 2022: 3,120+ participating companies61

September 2023: ~6,000 companies, ~645,000 employee records, 27,000 executive comp records62

2024: 8,500+ customers, 1M+ employee records, “Billions in compensation managed” via the platform63

Who buys the data

Pave primarily targets HR/finance teams. They focused heavily on startups and tech companies at first, where equity-heavy packages made the compensation problem the hardest. Pricing is seat based, based on # of employees the company has.

Competitors

The incumbents are Radford/Aon and Mercer (periodic surveys). The closest modern rivals are Carta Total Comp, which pulls equity data from 50,000+ cap tables, a structural data source Pave doesn’t have, and Ravio (European).64

Mission critical, temporal

Comp is analyzed on annual review cycles and re-benchmarked on every offer in the hiring market. The data decays fast, therefore the real-time feed is where the value lies. The data is mission-critical to a company’s hiring team, though lower-stakes (per decision) than a billion-dollar investment (ex. Preqin, Burgiss).

Pave’s potential acquirers

Pave is the only company of the six that has yet to be acquired. Every other business we covered was acquired by a larger player. Pave’s natural acquirers are the same kind of platform: an HRIS (Workday, ADP), Carta, or one of the legacy players (Aon/Radford, Mercer).

Brute force

GTG businesses often have to brute force their way into a position of authority to be able to gain access to data. It’s the classic chicken and the egg problem, why would anyone hand over their data before the dataset is worth anything? The answer, in all six cases, is that they led with a standalone product that was useful on day one, and let the data accumulate as a byproduct.

Ride a wave

GTG data businesses are levered to the size of the markets they index.

To test whether a GTG data business will either be riding a wave or running into a wall, we need to ask, where is the budget for the data coming from?

Burgiss and Preqin had different initial wedges (software vs. brute-forced FOIA), data philosophies (LP sourced vs. mixed), but both caught the wave of a more than 20x increase in private market AUM from 2000 to 2024. 65McKinsey:

As AUM increased, there were more LPs to sell to, more GPs to track, more funds raised, and a larger fee pool for buyers to pay for the data. The value of the benchmarks and data itself increased as more capital was being measured against them.

For STR, hotel room growth has been slow and steady. STR won based on market penetration more-so than riding huge growth in the hotel industry:66

Build on top of mission critical, temporal data

In a data business, generally, the more volatile and time sensitive the data is, the more valuable it is. This advantage cuts both ways, the faster data decays, the more a customer needs the live feed, and the less the historical corpus is worth (ex: Tegus historical corpus is arguably worth less than Burgiss/Preqin). From the businesses we covered:

Daily: hotel rates (STR). Pricing moves every night, so the feed is indispensable and the contract lock-in is deepest.

Per-offer / annual: compensation (Pave). Re-benchmarked on every hire/role.

Quarterly, lagged: fund performance (Burgiss, Preqin, eVestment). Slow-moving, but mission-critical. High historical value, since past performance is a strong signal for manager quality.

Short, non-compounding: expert transcripts (Tegus). A six-month-old call rarely matters, so the library doesn’t compound the way a benchmark does. Tegus’ data value depends on constantly updating its corpus.

The sweet spot is data that’s both temporal enough that customers can’t live without the latest information, and cumulative enough that the back catalog still has value.

GTG businesses are great acquisition targets

Five of the six businesses above sold, only Pave remains as an independent. The acquirers we covered bought a hole in their own coverage. CoStar owned every commercial real-estate vertical except hospitality, and they were able to plug that gap with the acquisition of STR. MSCI sold public-market benchmarks and had no private-market equivalent, until they found Burgiss. Nasdaq, BlackRock (Aladdin/eFront), and AlphaSense each bought a dataset that completed their platform. A GTG asset is worth more bolted onto distribution than standing alone, so the strategic buyer is in a strong position to bid it up. Second, the buyer is usually paying for the right to lay a data-currency moat on top of the GTG moat. MSCI likely valued its newfound ability to index private markets, the way it indexes public ones, more than Burgiss’ ~$90m of revenue. Owning the most complete, most accurate corpus is the only way to create benchmarks that the whole market is forced to reference.

A non-exhaustive map of other data co-ops and GTG businesses, by sector:

Insurance & risk: Verisk (ISO ClaimSearch, public), Valen Data Consortium (Insurity, ‘17), Verisk Financial Services / Argus (TransUnion, ‘22), LexisNexis C.L.U.E. (RELX), Equifax, Experian, TransUnion, The Work Number (Equifax).

Healthcare: Datavant (merged with Ciox under New Mountain, ‘21), Strata Decision Technology (Roper, ‘15), Claritev / fka MultiPlan (public, NYSE: CTEV), Change Healthcare (Optum / UnitedHealth, ‘22), Surescripts (consortium of pharmacies + PBMs), IQVIA / fka IMS Health (public), 340B ESP (Second Sight Solutions), Truveta (health-system consortium).

Real estate: RealPage (Thoma Bravo, ‘21), CoStar, CoreLogic / now Cotality (Stone Point + Insight), Black Knight (ICE, ‘23).

Consumer & retail: Nielsen (Elliott / Brookfield, ‘22), NielsenIQ / NIQ (Advent, IPO’d ‘25), Circana / fka IRI + NPD (Hellman & Friedman), Crisp (itself rolling up Lumidata, SetSight, Shelf Engine), Numerator (Vista).

Mobility, freight & energy: ATPCO (airline-owned consortium), Urgently / fka Otonomo (NASDAQ: ULY), CarFax (S&P Global via IHS Markit), DAT Freight & Analytics (Roper), Enverus, Wood Mackenzie (Veritas Capital, ‘23), S&P Global Platts, Argus Media (General Atlantic).

Compensation & workforce: Pave, Ravio, Payscale (Francisco Partners), Glassdoor (Recruit), Carta

Fraud & Misc.: Early Warning Services / Zelle (consortium of seven banks), Sardine / Sonar (independent), ChoicePoint (RELX / LexisNexis, ‘08), Seisint (RELX / LexisNexis, ‘04), Agri Stats (bad rep.), Farmer’s Business Network (independent), Catena-X (automotive data consortium), Athinia (Merck KGaA × Palantir JV).

https://www.sec.gov/newsroom/speeches-statements/gensler-2021-05-26

https://www.calpers.ca.gov/investments/investment-manager-opportunities/public-investment-manager-opportunities

https://www.jameskocis.com

James M. Kocis, James C. Bachman IV, Austin M. Long III, and Craig J. Nickels. Inside Private Equity: The Professional Investor’s Handbook. Wiley, 2009.

https://web.archive.org/web/19980203084035fw_/http://www.burgiss.com/scrcomm.html

https://web.archive.org/web/20100212120838/https://www.prweb.com/releases/2006/08/prweb429766.htm

https://www.prnewswire.com/news-releases/burgiss-announces-major-release-of-private-i-its-flagship-product-300362134.html

https://www.prnewswire.com/news-releases/burgiss-advances-private-i-platform-300613866.html

https://ir.msci.com/news-releases/news-release-details/msci-and-burgiss-enter-strategic-relationship

https://ir.msci.com/static-files/25656e42-b93b-4c46-8c3b-5d28a88875b9

https://www.businesswire.com/news/home/20211004005221/en/Burgiss-and-Caissa-Complete-Merger

https://www.msci.com/documents/10199/1107902a-7ab6-81f4-240e-c125cddb2520

https://ir.msci.com/news-releases/news-release-details/msci-announces-acquisition-burgiss-expanding-private-assets

https://www.msci.com/documents/1296102/47386594/MSCI+Private+Capital+Closed-end+Fund+Indexes.pdf/79d9f60b-69c1-757a-67f6-c686f82c61cd

https://www.nber.org/system/files/chapters/c13495/revisions/c13495.rev2.pdf

https://fortune.com/europe/2024/07/05/uk-latest-billionaire-sharing-650-million-employees-selling-data-company

https://en.wikipedia.org/wiki/Preqin

https://www.preqin.com/about/press-release/blackrock-to-acquire-preqin-leading-private-markets-data-solutions-provider

https://s24.q4cdn.com/856567660/files/doc_events/2024/BLK-Preqin-Press-Release.pdf

https://docs.preqin.com/pro/Private-Capital-Performance-Guide.pdf

https://www.kenaninstitute.unc.edu/wp-content/uploads/2017/03/PERC_datasets_12-5-2015.pdf

https://www.blackrock.com/aladdin/discover/blackrock-to-acquire-preqin

https://archive.is/20240701135735/https://www.bloomberg.com/news/articles/2024-07-01/blackrock-aims-to-index-the-private-markets-after-preqin-deal

https://www.financedirectoreurope.com/news/msci-to-take-full-ownership-of-burgiss-in-697m-deal/

https://s24.q4cdn.com/856567660/files/doc_events/2024/BLK-Preqin-Investor-Presentation.pdf

https://ir.msci.com/news-releases/news-release-details/msci-announces-acquisition-burgiss-expanding-private-assets

https://mag.hospitalityupgrade.com/publication/frame.php?i=625192&p=&pn=&ver=html5&view=articleBrowser&article_id=3499523

https://business.cornell.edu/hub/2020/01/28/randell-smith-2020-hospitality-icon/

https://www.costar.com/article/1963354920/research-experts-launch-str-global

https://www.costargroup.com/press-room/2019/costar-group-acquire-str-global-leader-benchmarking-analytics-hospitality-industry

https://storage.courtlistener.com/recap/gov.uscourts.wawd.331643/gov.uscourts.wawd.331643.1.0.pdf

https://mag.hospitalityupgrade.com/publication/frame.php?i=625192&p=&pn=&ver=html5&view=articleBrowser&article_id=3499523

https://www.hospitalitynet.org/opinion/4045406/thank-you-for-helping-create-our-brand

https://www.costar.com/products/str-benchmark/resources/guidelines/competitive-set-guidelines

https://www.costar.com/en-gb/what-average-daily-rate-adr-and-how-calculate-it

https://www.costar.com/en-gb/what-average-daily-rate-adr-and-how-calculate-it

https://storage.courtlistener.com/recap/gov.uscourts.wawd.331643/gov.uscourts.wawd.331643.1.0.pdf

https://www.costar.com/article/280004942/costar-to-buy-str-for-450-million

https://inex.one/expert-network-directory/tegus-expert-network

https://www.prnewswire.com/news-releases/tegus-acquires-bamsec-to-deliver-financial-filings-and-earnings-calls-through-its-business-intelligence-platform-301408392.html

https://canalyst.com/blog/tegus-acquires-canalyst/

https://www.prnewswire.com/news-releases/alphasense-completes-acquisition-of-tegus-302190934.html

https://www.prnewswire.com/news-releases/alphasense-to-join-forces-with-tegus-increases-latest-valuation-to-4b-302169502.html

https://growthcapadvisory.com/the-true-growth-entrepreneur-jim-minnick/

https://web.archive.org/web/20140330171352/https://www.evestment.com/products/omni

https://ir.nasdaq.com/news-releases/news-release-details/nasdaq-acquire-evestment

https://ir.west.com/static-files/14a64e64-2e3d-453d-94a6-e171fc8b717d

https://web.archive.org/web/20140330171112/https://www.evestment.com/submit-my-data

https://www.calpers.ca.gov/investments/investment-manager-opportunities/public-investment-manager-opportunities

https://www.nasdaq.com/docs/asset-owner-solutions-italian-pension-case-study

https://www.pave.com/products/market-data-methodology

https://web.archive.org/web/20220524080846/https://www.beondeck.com/case-studies/matt-schulman

https://web.archive.org/web/20200826095911/https://www.trytrove.co/

https://www.linkedin.com/in/matt-schulman-15911861/

https://www.businesswire.com/news/home/20201203005339/en/Trove-Raises-%2416-Million-Series-A-Led-By-Andreessen-Horowitz-Unveils-Rebrand-To-Pave

https://www.pave.com/products/market-data-methodology

https://pitchbook.com/newsletter/pave-picks-up-46m-series-b

https://www.pave.com/blog-posts/acquiring-option-impact-and-the-future-of-startup-compensation-data

https://web.archive.org/web/20220929213705/https://www.pave.com/products/compensation-benchmarking-data

https://research.contrary.com/company/pave

https://www.pave.com/blog-posts/2024-pave-platform-rewind-billions-in-compensation-delivered

https://carta.com/carta-vs-pave/

https://www.mckinsey.com/~/media/mckinsey/industries/private%20equity%20and%20principal%20investors/our%20insights/mckinseys%20global%20private%20markets%20report/2025/global-private-markets-report-2025-braced-for-shifting-weather.pdf

https://www.costar.com/article/1741863595/why-2025-could-be-a-pivotal-year-for-us-hotels